Accounting and tax support in Japan is provided by certified public accountants and tax accountants. The role of certified public accountants is to perform audits under the Certified Public Accountant Law, while tax accountants engage in typical tax agent services such as the preparation of tax documentation and giving tax consultations under the Certified Tax Accountant Law. Additionally, both professions provide additional services such as business consulting.

Not only accounting principles but also taxation systems will differ profoundly, depending upon the status of the business entity which can vary from representative or branch office over the typical 100% subsidiary as permanent establishment called Kabushiki Kaisha to the lesser known Limited Liability Company / Godoh Kaisha (LLC/GK) and Limited Liability Partnership (LLP).

All basic accounting principles for any domestic company are based upon the following seven pillars namely;

- true and fair reporting,

- an orderly system of bookkeeping,

- a distinction between capital surplus and earned surplus,

- a clear disclosure,

- consistency,

- prudence and

- in accordance with reliable accounting records and facts.

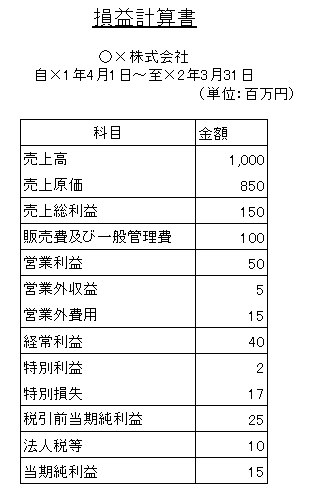

Financial documents of a fiscal year closing usually consists of the following documents being, the Balance Sheet (B/S) (taishakutaishohyou), the Profit and Loss statement (P/L) (sonekikeisansho), the statement of changes in net corporate assets (kabunushi shihon touhen doukei sansho) and where needed, also explanatory notes for the aforesaid financial statements.

{kind=link}

Consumption tax is a national tax levied against the volume of business and through self-assessment. The consumption tax rate has been raised to 10% since October 1st, 2019 for most goods and services. This 10% includes a 2.2% local consumption tax rate. The reduced tax rate of 8% (local consumption tax, 1.76%) is applied to sales of food and beverages, except for alcoholic drinks and dining out, and sales of newspapers published more than twice a week (under subscription contracts). This raise has been decided as a measure to help reduce the national debt.

Domestic transactions subject to consumption tax include the transfer or rental of assets or the provision of services as a business in Japan by an enterprise. Import transactions such as cargo retrieved from a bonded zone are also liable.

- The Consumption tax rate in Japan is 10%, except for food stuffs which is 8%

- It has to be collected and paid between businesses (B2B transactions)

- The amount paid during B2B transactions is compensated by the amount collected during sales

- Price tags have to include the Consumption tax amount

- For businesses without taxable sales in Japan, a refund of CT paid in Japan is not possible.

Under the Japanese Consumption Tax Law (JCT), small enterprises with taxable sales of ¥10 million or less in the base period (e.g. the period two terms prior to the current tax year) do not need to file a CT return. This is only an exemption from filing, and as such, tax-exempt companies are still required to pay JCT to the vendor or service supplier when purchases are made.

Similarly, the JCT Law does not prohibit tax-exempt enterprises from charging CT to its customers. Tax-exempt enterprises are, in effect, allowed to keep the collected taxes minus the CT on purchases. For some businesses this may result in significant windfalls, although these are subject to corporate income tax.

We will carefully examine your business in order to provide the best consumption tax advice. If you are manufacturing or you export a lot, structuring your tax in the right way can result in considerable savings and refunds.